Coding#

import yfinance as yf

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

import statistics

from sklearn.metrics import accuracy_score

Data#

The following function returns a tuple containing the training and test datasets for a specified stock and time period.

The training_ratio parameter represents the percentage of data allocated to the training set.

def get_training_test_data(stock='AMZN', start='2019-1-1', end='2021-1-31', training_ratio=0.96):

df = yf.Ticker(stock).history(start=start, end=end)

df = df.iloc[:,:-3]

df.reset_index(inplace=True)

df['Date'] = [i.date() for i in df.Date]

df['fcc'] = [np.sign(df.Close.loc[i+1]-df.Close.loc[i]) for i in range(len(df)-1)]+[np.nan]

training_length = int(len(df)*training_ratio)

training_data = df.iloc[:training_length,:]

test_data = df.iloc[training_length:,:]

test_data.reset_index(inplace=True, drop=True)

return (training_data, test_data)

df_train, df_test = get_training_test_data()

df_train.shape, df_test.shape

---------------------------------------------------------------------------

YFRateLimitError Traceback (most recent call last)

Cell In[3], line 1

----> 1 df_train, df_test = get_training_test_data()

2 df_train.shape, df_test.shape

Cell In[2], line 2, in get_training_test_data(stock, start, end, training_ratio)

1 def get_training_test_data(stock='AMZN', start='2019-1-1', end='2021-1-31', training_ratio=0.96):

----> 2 df = yf.Ticker(stock).history(start=start, end=end)

3 df = df.iloc[:,:-3]

4 df.reset_index(inplace=True)

File ~/anaconda3/lib/python3.11/site-packages/yfinance/utils.py:104, in log_indent_decorator.<locals>.wrapper(*args, **kwargs)

101 logger.debug(f'Entering {func.__name__}()')

103 with IndentationContext():

--> 104 result = func(*args, **kwargs)

106 logger.debug(f'Exiting {func.__name__}()')

107 return result

File ~/anaconda3/lib/python3.11/site-packages/yfinance/base.py:80, in TickerBase.history(self, *args, **kwargs)

78 @utils.log_indent_decorator

79 def history(self, *args, **kwargs) -> pd.DataFrame:

---> 80 return self._lazy_load_price_history().history(*args, **kwargs)

File ~/anaconda3/lib/python3.11/site-packages/yfinance/utils.py:104, in log_indent_decorator.<locals>.wrapper(*args, **kwargs)

101 logger.debug(f'Entering {func.__name__}()')

103 with IndentationContext():

--> 104 result = func(*args, **kwargs)

106 logger.debug(f'Exiting {func.__name__}()')

107 return result

File ~/anaconda3/lib/python3.11/site-packages/yfinance/scrapers/history.py:175, in PriceHistory.history(self, period, interval, start, end, prepost, actions, auto_adjust, back_adjust, repair, keepna, proxy, rounding, timeout, raise_errors)

173 get_fn = self._data.cache_get

174 try:

--> 175 data = get_fn(

176 url=url,

177 params=params,

178 proxy=proxy,

179 timeout=timeout

180 )

181 if "Will be right back" in data.text or data is None:

182 raise RuntimeError("*** YAHOO! FINANCE IS CURRENTLY DOWN! ***\n"

183 "Our engineers are working quickly to resolve "

184 "the issue. Thank you for your patience.")

File ~/anaconda3/lib/python3.11/site-packages/yfinance/data.py:32, in lru_cache_freezeargs.<locals>.wrapped(*args, **kwargs)

30 args = tuple([tuple(arg) if isinstance(arg, list) else arg for arg in args])

31 kwargs = {k: tuple(v) if isinstance(v, list) else v for k, v in kwargs.items()}

---> 32 return func(*args, **kwargs)

File ~/anaconda3/lib/python3.11/site-packages/yfinance/data.py:416, in YfData.cache_get(self, url, user_agent_headers, params, proxy, timeout)

413 @lru_cache_freezeargs

414 @lru_cache(maxsize=cache_maxsize)

415 def cache_get(self, url, user_agent_headers=None, params=None, proxy=None, timeout=30):

--> 416 return self.get(url, user_agent_headers, params, proxy, timeout)

File ~/anaconda3/lib/python3.11/site-packages/yfinance/utils.py:104, in log_indent_decorator.<locals>.wrapper(*args, **kwargs)

101 logger.debug(f'Entering {func.__name__}()')

103 with IndentationContext():

--> 104 result = func(*args, **kwargs)

106 logger.debug(f'Exiting {func.__name__}()')

107 return result

File ~/anaconda3/lib/python3.11/site-packages/yfinance/data.py:347, in YfData.get(self, url, user_agent_headers, params, proxy, timeout)

345 @utils.log_indent_decorator

346 def get(self, url, user_agent_headers=None, params=None, proxy=None, timeout=30):

--> 347 return self._make_request(url, request_method = self._session.get, user_agent_headers=user_agent_headers, params=params, proxy=proxy, timeout=timeout)

File ~/anaconda3/lib/python3.11/site-packages/yfinance/utils.py:104, in log_indent_decorator.<locals>.wrapper(*args, **kwargs)

101 logger.debug(f'Entering {func.__name__}()')

103 with IndentationContext():

--> 104 result = func(*args, **kwargs)

106 logger.debug(f'Exiting {func.__name__}()')

107 return result

File ~/anaconda3/lib/python3.11/site-packages/yfinance/data.py:409, in YfData._make_request(self, url, request_method, user_agent_headers, body, params, proxy, timeout)

407 # Raise exception if rate limited

408 if response.status_code == 429:

--> 409 raise YFRateLimitError()

411 return response

YFRateLimitError: Too Many Requests. Rate limited. Try after a while.

df_train.head()

| Date | Open | High | Low | Close | fcc | |

|---|---|---|---|---|---|---|

| 0 | 2019-01-02 | 73.260002 | 77.667999 | 73.046501 | 76.956497 | -1.0 |

| 1 | 2019-01-03 | 76.000504 | 76.900002 | 74.855499 | 75.014000 | 1.0 |

| 2 | 2019-01-04 | 76.500000 | 79.699997 | 75.915497 | 78.769501 | 1.0 |

| 3 | 2019-01-07 | 80.115501 | 81.727997 | 79.459503 | 81.475502 | 1.0 |

| 4 | 2019-01-08 | 83.234497 | 83.830498 | 80.830498 | 82.829002 | 1.0 |

df_test.head()

| Date | Open | High | Low | Close | fcc | |

|---|---|---|---|---|---|---|

| 0 | 2020-12-30 | 167.050003 | 167.104996 | 164.123505 | 164.292496 | -1.0 |

| 1 | 2020-12-31 | 163.750000 | 164.145996 | 162.059998 | 162.846497 | -1.0 |

| 2 | 2021-01-04 | 163.500000 | 163.600006 | 157.201004 | 159.331497 | 1.0 |

| 3 | 2021-01-05 | 158.300507 | 161.169006 | 158.253006 | 160.925507 | -1.0 |

| 4 | 2021-01-06 | 157.324005 | 159.875504 | 156.557999 | 156.919006 | 1.0 |

Visualization#

def cs_visualize(hp, op, cp, lp, x=0, details=False, linewidth=20):

if cp > op: color = 'green'

elif cp < op: color = 'red'

else: color ='black'

plt.plot([x,x], [lp, hp], c=color)

if cp != op:

plt.plot([x,x], [op, cp], c=color, linewidth=linewidth)

else:

plt.plot([x-0.1,x+0.1], [op, cp], c=color, linewidth=1)

if details:

plt.text(x+0.01, hp, 'high')

plt.text(x+0.01, lp , 'low')

plt.text(x+0.01, cp, 'close')

plt.text(x+0.01, op, 'open')

def cs_visualize_df(data, M=0, N=None):

plt.figure(figsize=(20,5))

for i in data.index[M:N]:

hp, op, cp, lp = data[['High','Open', 'Close', 'Low']].loc[i]

cs_visualize(hp, op, cp, lp, x=i)

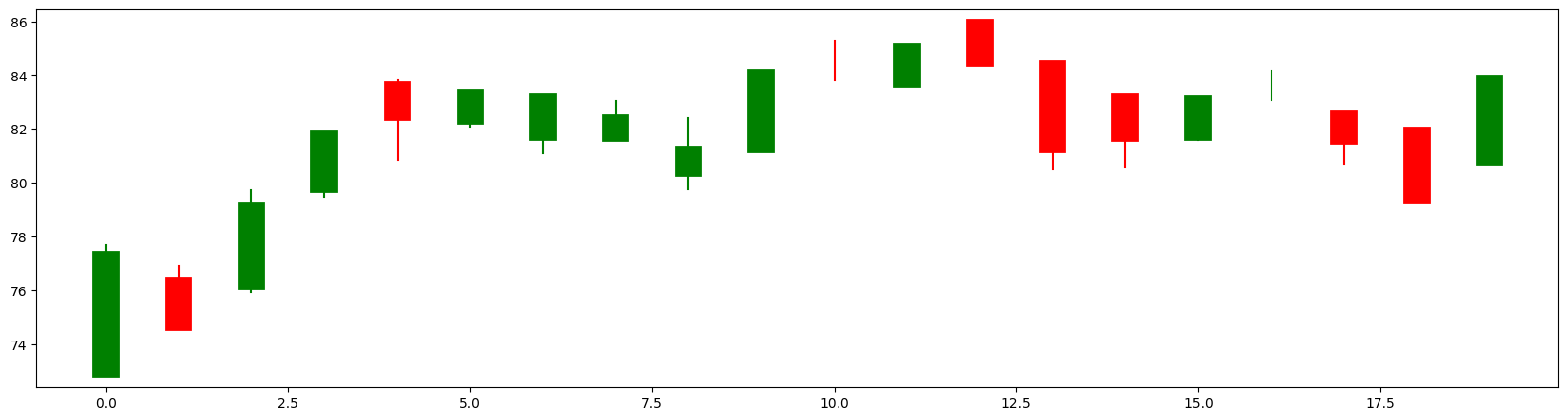

cs_visualize_df(df_train, M=0, N=20)

Encoding#

def encoder(hp, op, cp, lp):

if hp > op > cp > lp: return 'a'

if hp == op > cp > lp: return 'b'

if hp == op > cp == lp: return 'c'

if hp > op > cp == lp: return 'd'

if hp > cp > op > lp: return 'e'

if hp == cp > op > lp: return 'f'

if hp == cp > op == lp: return 'g'

if hp > cp > op == lp: return 'h'

if hp > op == cp > lp: return 'i'

if hp == op == cp > lp: return 'j'

if hp == op == cp == lp: return 'k'

if hp > op == cp == lp: return 'l'

def df_encoder(data):

data_ = data.copy()

encoder_list = []

for i in data_.index:

hp, op, cp, lp = data_[['High','Open', 'Close', 'Low']].loc[i]

encoder_list.append(encoder(hp, op, cp, lp))

data_['code'] = encoder_list

return data_

df_train = df_encoder(df_train)

df_train.head().round(2)

| Date | Open | High | Low | Close | fcc | code | |

|---|---|---|---|---|---|---|---|

| 0 | 2019-01-02 | 73.26 | 77.67 | 73.05 | 76.96 | -1.0 | e |

| 1 | 2019-01-03 | 76.00 | 76.90 | 74.86 | 75.01 | 1.0 | a |

| 2 | 2019-01-04 | 76.50 | 79.70 | 75.92 | 78.77 | 1.0 | e |

| 3 | 2019-01-07 | 80.12 | 81.73 | 79.46 | 81.48 | 1.0 | e |

| 4 | 2019-01-08 | 83.23 | 83.83 | 80.83 | 82.83 | 1.0 | a |

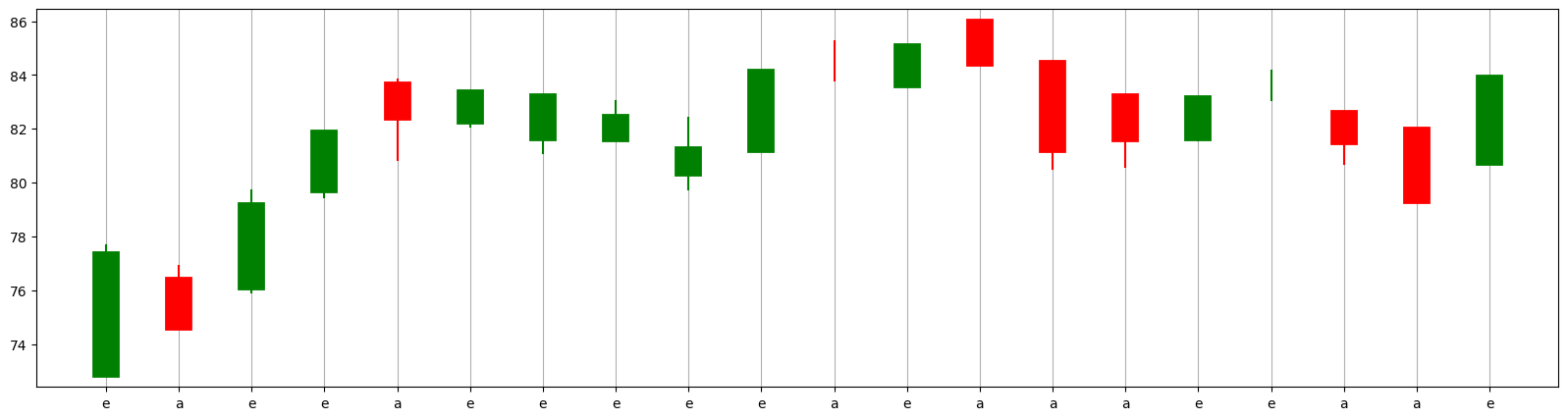

The chart below illustrates the candlestick charts along with their corresponding codes.

cs_visualize_df(df_train, M=0, N=20)

plt.xticks(range(0,20), df_train.code[0:20])

plt.grid(axis='x');

Change Points#

def change_points(data):

data_ = data.copy()

change_pts, change_types = [True], ['Start']

for i in range(1, len(data_)-1):

left_change = int(np.sign(data_['Close'][i]-data_['Close'][i-1]))

right_change = int(np.sign(data_['Close'][i+1]-data_['Close'][i]))

if left_change != right_change:

change_pts.append(True)

else:

change_pts.append(False)

change_types.append((left_change, right_change))

change_pts.append(False)

change_types.append('End')

data_['change_points'] = change_pts

data_['change_types'] = change_types

return data_

df_train = change_points(df_train)

df_train.head().round(2)

| Date | Open | High | Low | Close | fcc | code | change_points | change_types | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 2019-01-02 | 73.26 | 77.67 | 73.05 | 76.96 | -1.0 | e | True | Start |

| 1 | 2019-01-03 | 76.00 | 76.90 | 74.86 | 75.01 | 1.0 | a | True | (-1, 1) |

| 2 | 2019-01-04 | 76.50 | 79.70 | 75.92 | 78.77 | 1.0 | e | False | (1, 1) |

| 3 | 2019-01-07 | 80.12 | 81.73 | 79.46 | 81.48 | 1.0 | e | False | (1, 1) |

| 4 | 2019-01-08 | 83.23 | 83.83 | 80.83 | 82.83 | 1.0 | a | False | (1, 1) |

df_train = change_points(df_train)

df_train.tail().round(2)

| Date | Open | High | Low | Close | fcc | code | change_points | change_types | |

|---|---|---|---|---|---|---|---|---|---|

| 498 | 2020-12-22 | 160.14 | 161.10 | 159.00 | 160.33 | -1.0 | e | True | (1, -1) |

| 499 | 2020-12-23 | 160.25 | 160.51 | 159.21 | 159.26 | -1.0 | a | False | (-1, -1) |

| 500 | 2020-12-24 | 159.70 | 160.10 | 158.45 | 158.63 | 1.0 | a | True | (-1, 1) |

| 501 | 2020-12-28 | 159.70 | 165.20 | 158.63 | 164.20 | 1.0 | e | False | (1, 1) |

| 502 | 2020-12-29 | 165.50 | 167.53 | 164.06 | 166.10 | -1.0 | e | False | End |

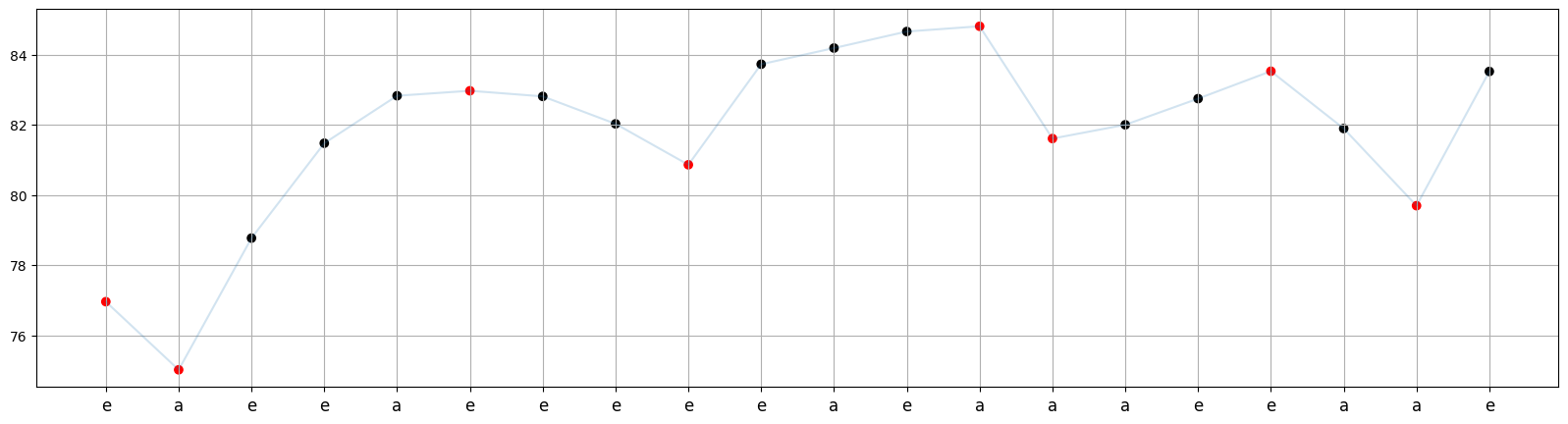

def cp_visualizer(data, M=0, N=None):

plt.figure(figsize=(20,5))

plt.plot(data.index[M:N], data.Close[M:N], alpha=0.2)

color_list = ['black', 'red']

plt.scatter(data.index[M:N], data.Close[M:N], c=[color_list[i] for i in data.change_points[M:N]])

plt.xticks(data.index[M:N], data.code[M:N], fontsize=12)

plt.grid();

In the graph of Close values below, the red points indicate the change points, while the x-values correspond to the candlestick code for each corresponding day.

cp_visualizer(df_train, M=0, N=20)

Segmentation and Labeling#

def segmentation(data):

segment_list, trend_list = [], []

pattern = ''

for i in range(len(data)-1):

pattern += data.code[i]

if data.change_points.loc[i]:

segment_list.append(pattern)

j = i

while True:

if data.change_types[j+1][0] != 0: # first non-equal direction

trend_list.append(data.change_types[j+1][0])

break

j += 1

pattern = ''

df_seg = pd.DataFrame()

df_seg['kts'] = segment_list

df_seg['trend'] = trend_list

df_seg_unique = pd.DataFrame(df_seg.value_counts()).reset_index()

return df_seg_unique

PSet = segmentation(df_train)

PSet.head()

| kts | trend | count | |

|---|---|---|---|

| 0 | a | 1 | 58 |

| 1 | e | -1 | 47 |

| 2 | aa | 1 | 23 |

| 3 | ee | -1 | 15 |

| 4 | e | 1 | 9 |

Subsequence#

def whethersub(X, Y):

if len(X) > len(Y): return 0

else:

k = 0

for i in range(len(X)):

if X[i] in Y[k:]:

k = Y.find(X[i], k)+1

else:

return 0

return 1

oNum#

def onum(pset):

pset_ = pset.copy()

onum_list = []

for i in range(len(pset)):

total = 0

for j in range(len(pset)):

total += whethersub(pset_.loc[i, 'kts'], pset_.loc[j, 'kts'])* pset_.loc[j, 'count']

onum_list.append(total)

pset_['onum'] = onum_list

return pset_

PRSet = onum(PSet)

PRSet.head()

| kts | trend | count | onum | |

|---|---|---|---|---|

| 0 | a | 1 | 58 | 154 |

| 1 | e | -1 | 47 | 146 |

| 2 | aa | 1 | 23 | 58 |

| 3 | ee | -1 | 15 | 60 |

| 4 | e | 1 | 9 | 146 |

sameTrendNum#

def sametrendnum(pset):

pset_ = pset.copy()

sametrendnum_list = []

for i in range(len(pset_)):

total = 0

for j in range(len(pset_)):

if whethersub(pset_.loc[i,'kts'], pset_.loc[j,'kts']) & (pset_.loc[i,'trend'] == pset_.loc[j, 'trend']):

total += pset_.loc[j, 'count']

sametrendnum_list.append(total)

pset_['sametrendnum'] = sametrendnum_list

return pset_

PRSet = sametrendnum(PRSet)

PRSet.head()

| kts | trend | count | onum | sametrendnum | |

|---|---|---|---|---|---|

| 0 | a | 1 | 58 | 154 | 111 |

| 1 | e | -1 | 47 | 146 | 115 |

| 2 | aa | 1 | 23 | 58 | 47 |

| 3 | ee | -1 | 15 | 60 | 56 |

| 4 | e | 1 | 9 | 146 | 31 |

PACC#

def pacc(pset):

pset_ = pset.copy()

pset_['pacc'] = pset_['sametrendnum'] / pset_['onum']

return pset_

PRSet = pacc(PRSet)

PRSet.head().round(2)

| kts | trend | count | onum | sametrendnum | pacc | |

|---|---|---|---|---|---|---|

| 0 | a | 1 | 58 | 154 | 111 | 0.72 |

| 1 | e | -1 | 47 | 146 | 115 | 0.79 |

| 2 | aa | 1 | 23 | 58 | 47 | 0.81 |

| 3 | ee | -1 | 15 | 60 | 56 | 0.93 |

| 4 | e | 1 | 9 | 146 | 31 | 0.21 |

The set described above is called the Pattern Record Set (PRSet).

It consists of KTS-Trend pairs (KtsP) and their corresponding Pattern Accuracy Score (PACC) values.

Subsequence Model#

def subsequence_model_predict(kts, prset):

best_pattern = []

best_pacc = [0]

best_trend = []

for i in range(len(prset)):

if (whethersub(prset.loc[i, 'kts'], kts)):

if prset.loc[i, 'pacc'] > best_pacc[-1]:

best_pattern = [prset.loc[i, 'kts']]

best_pacc = [prset.loc[i, 'pacc']]

best_trend = [ prset.loc[i, 'trend']]

elif prset.loc[i, 'pacc'] == best_pacc[-1]:

best_pattern.append(prset.loc[i, 'kts'])

best_pacc.append(prset.loc[i, 'pacc'])

best_trend.append(prset.loc[i, 'trend'])

if len(best_trend) == 0:

pred = statistics.mode(prset.trend)

elif len(best_trend) == 1:

pred = best_trend[0]

else:

pred = statistics.mode(best_trend)

return {'Best Pattern':best_pattern, 'Best PACC': best_pacc, 'Best Trend': best_trend, 'Prediction':pred}

subsequence_model_predict('aaee', PRSet)

{'Best Pattern': ['ee'],

'Best PACC': [0.9333333333333333],

'Best Trend': [-1],

'Prediction': -1}

subsequence_model_predict('acd', PRSet)

{'Best Pattern': ['a'],

'Best PACC': [0.7207792207792207],

'Best Trend': [1],

'Prediction': 1}

Test Set#

df_test.head().round(2)

| Date | Open | High | Low | Close | fcc | |

|---|---|---|---|---|---|---|

| 0 | 2020-12-30 | 167.05 | 167.10 | 164.12 | 164.29 | -1.0 |

| 1 | 2020-12-31 | 163.75 | 164.15 | 162.06 | 162.85 | -1.0 |

| 2 | 2021-01-04 | 163.50 | 163.60 | 157.20 | 159.33 | 1.0 |

| 3 | 2021-01-05 | 158.30 | 161.17 | 158.25 | 160.93 | -1.0 |

| 4 | 2021-01-06 | 157.32 | 159.88 | 156.56 | 156.92 | 1.0 |

df_test = df_encoder(df_test)

df_test.head().round(2)

| Date | Open | High | Low | Close | fcc | code | |

|---|---|---|---|---|---|---|---|

| 0 | 2020-12-30 | 167.05 | 167.10 | 164.12 | 164.29 | -1.0 | a |

| 1 | 2020-12-31 | 163.75 | 164.15 | 162.06 | 162.85 | -1.0 | a |

| 2 | 2021-01-04 | 163.50 | 163.60 | 157.20 | 159.33 | 1.0 | a |

| 3 | 2021-01-05 | 158.30 | 161.17 | 158.25 | 160.93 | -1.0 | e |

| 4 | 2021-01-06 | 157.32 | 159.88 | 156.56 | 156.92 | 1.0 | a |

def test_data_prep(data, N=5):

test_data = []

for i in range(len(data)-N):

kts = ''

for j in range(N):

kts += data.code.loc[i+j]

test_data.append((kts, data.fcc.loc[i+j]))

if type(test_data[-1][-1]) != float:

test_data.pop()

return test_data

test_data = test_data_prep(df_test)

test_data

[('aaaea', 1.0),

('aaeae', 1.0),

('aeaee', -1.0),

('eaeea', 1.0),

('aeeae', 1.0),

('eeaee', -1.0),

('eaeea', -1.0),

('aeeaa', 1.0),

('eeaae', 1.0),

('eaaee', 1.0),

('aaeee', -1.0),

('aeeea', 1.0),

('eeeaa', 1.0),

('eeaae', -1.0),

('eaaea', 1.0)]

Prediction#

def subsequence_model_score(data, prset):

pred_trend_test = [subsequence_model_predict(kts, prset)['Prediction'] for (kts,trend) in data]

actual_trend_test = [trend for (kts,trend) in data]

return accuracy_score(pred_trend_test, actual_trend_test)

subsequence_model_score(test_data, PRSet)

0.6